Working with independent contractors outside the United States is a normal part of running a small business. Millions of legitimate cross-border payments happen every day—covering everything from web development and design to marketing, translation, and consulting. Global sourcing is common, and the payments themselves are legal and straightforward for most businesses.

Where confusion tends to arise is on the tax and documentation side. When you pay a domestic contractor, you likely know the drill: collect a W-9, issue a 1099-NEC at year-end. But what happens when your contractor is based in another country? The rules are different—and often simpler than you might expect.

The key isn’t avoiding international contractor payments. It’s having a simple, consistent process in place. With the right documentation and a clear understanding of IRS requirements, paying foreign independent contractors can be uncomplicated and fully compliant.

This article is for informational purposes only and does not constitute tax or legal advice. Consult a qualified tax professional for guidance specific to your situation.

Step 1: Determine the Contractor’s Tax Status

Before anything else, you need to establish whether your contractor is a U.S. person or a foreign person in the eyes of the IRS. This distinction drives everything that follows.

Is the Contractor a U.S. Person or a Foreign Person?

A U.S. person includes U.S. citizens and resident aliens—regardless of where they currently live. A foreign person is generally a nonresident alien individual or a foreign business entity.

Here’s the important nuance: tax status is not the same as physical location. A U.S. citizen living in Germany is still a U.S. person for IRS purposes. A contractor based in Canada is a foreign person. Getting this right from the start keeps your documentation on track.

Step 2: Collect the Correct Tax Form

The form you collect depends on who your contractor is. Make a habit of requesting this before issuing your first payment.

Form W-9 (For U.S. Persons)

If your contractor is a U.S. person—even one working abroad—collect a Form W-9. This is the standard form used to issue a 1099-NEC at year-end.

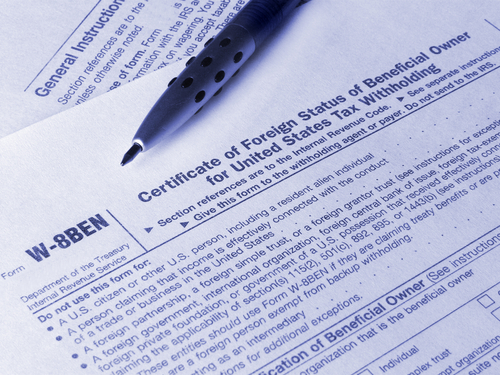

Form W-8BEN (For Foreign Individuals)

For individual contractors who are foreign persons, collect a Form W-8BEN. This form certifies their foreign status and confirms that payments to them fall outside standard 1099 reporting rules.

Form W-8BEN-E (For Foreign Entities)

If you’re contracting with a foreign business rather than an individual, request a Form W-8BEN-E instead. The same principle applies—it certifies the entity’s foreign status for tax purposes.

Collecting the right form upfront is the single most important step in the entire process.

Do You Issue a 1099 to Foreign Contractors?

In most cases, no. If your contractor is a non-U.S. person and the services are performed outside the United States, you are generally not required to issue a 1099-NEC.

There are two notable exceptions worth knowing:

- U.S. citizens living abroad are still U.S. persons and should receive a 1099-NEC just as they would if they lived stateside.

- Services performed inside the United States, even by a foreign person, may trigger different reporting requirements.

If either of these situations applies to you, consult with a tax professional to confirm your obligations.

Are You Required to Withhold Taxes?

For many small businesses paying foreign contractors, withholding is not required. But the answer depends on where the work is actually performed.

Services Performed Outside the U.S.

When a foreign contractor performs services entirely outside the United States, payments are generally not subject to U.S. withholding. This covers the majority of international contractor arrangements.

Services Performed Inside the U.S.

If a foreign contractor performs work while physically present in the U.S., the rules change. Withholding may apply, and additional forms such as Form 1042 and Form 1042-S may be required. This is one of the clearer situations where professional tax guidance is worth the investment.

What About Backup Withholding?

Backup withholding is a mechanism that applies when a payer cannot confirm a payee’s tax status—typically because proper documentation was never collected. The standard backup withholding rate is 24%.

The good news: collecting a signed W-8BEN or W-8BEN-E from your foreign contractor generally prevents backup withholding from applying. This is another reason why gathering the correct form before payment matters.

Recordkeeping Requirements

Good documentation is what protects your business if questions ever arise. Keep the following organized and accessible:

Maintain Signed W-8 or W-9 Forms

Store these in your vendor records as soon as you receive them. A W-8BEN is typically valid for three years, unless your contractor’s circumstances change.

Keep Contractor Agreements

A written contract or statement of work clarifies the scope of services, payment terms, and—critically—where the work is performed.

Save Invoices and Payment Records

Every invoice and payment confirmation should be retained. This supports accurate bookkeeping and gives you a clear audit trail.

Track Where Services Were Performed

Location matters for withholding and reporting purposes. If your contractor works remotely from abroad, note that consistently in your records.

Common Mistakes Small Businesses Make

Knowing what to avoid is just as useful as knowing what to do.

Not Collecting a W-8 Before Payment

This is the most common oversight. Without it, you may face unnecessary backup withholding obligations or documentation gaps later.

Assuming Location Equals Tax Status

A contractor’s mailing address doesn’t determine their IRS classification. A U.S. citizen living in another country is still a U.S. person—and needs a W-9, not a W-8.

Issuing a 1099 Incorrectly

Sending a 1099-NEC to a foreign contractor who doesn’t need one can create unnecessary confusion. Confirming tax status first prevents this.

Overlooking Where Services Were Performed

Businesses sometimes focus entirely on the contractor’s residency and forget that the location of the work itself also affects reporting and withholding rules.

Simple Compliance Checklist

When onboarding a new foreign contractor, work through this list:

- Confirm the contractor’s tax residency (U.S. person or foreign person?)

- Collect W-8BEN (individuals) or W-8BEN-E (entities) from foreign persons

- Collect W-9 from U.S. persons, including U.S. citizens living abroad

- Determine where the services will be performed

- Document everything: contracts, invoices, payment confirmations

- Consult a tax professional if you’re uncertain about withholding obligations

When to Seek Professional Advice

Most foreign contractor situations are routine and manageable. But there are specific circumstances where professional guidance pays for itself:

- Your contractor will perform any work while physically inside the United States

- Payments are substantial, ongoing, or involve a complex contract structure

- You’ve received conflicting or incomplete documentation from the contractor

- You’re uncertain about withholding obligations for your specific arrangement

A qualified tax professional can help you navigate these cases quickly—and with confidence.

Frequently Asked Questions

Do I issue a 1099 to a foreign contractor?

Generally, no. If the contractor is a non-U.S. person and services are performed outside the United States, a 1099-NEC is not required. Exceptions apply for U.S. citizens abroad and for services performed inside the U.S.

What form should I collect from a foreign independent contractor?

Collect Form W-8BEN for foreign individuals, or Form W-8BEN-E if the contractor is a foreign business entity.

Do I need to withhold taxes when paying foreign contractors?

In many cases, no—provided services are performed outside the U.S. and you have a valid W-8 form on file. Situations involving work performed inside the U.S. may require withholding.

What happens if I don’t collect a W-8 form?

Without proper documentation, you may be subject to backup withholding obligations and face compliance complications. Collecting the form before payment is the simplest way to avoid this.

How long is a W-8BEN valid?

Typically three years from the date it’s signed, unless the contractor’s tax circumstances change before that period ends.