Hiring contractors outside the United States has become standard practice for many small businesses. Whether you’re working with a graphic designer in Brazil or a software developer in the Philippines, cross-border hiring opens the door to global talent. With that comes a reasonable question: do the same IRS reporting rules apply?

If you’re used to issuing Form 1099-NEC to domestic contractors, you might assume the process works the same for international ones. In most cases, it doesn’t. U.S. businesses are generally not required to issue a 1099 to foreign contractors — but that doesn’t mean documentation is optional. Knowing what’s required, and what to collect instead, keeps your business compliant and your records clean.

This guide breaks it down simply, so you can pay international contractors with confidence.

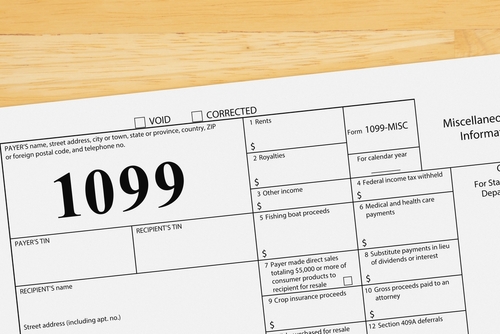

What Is Form 1099-NEC?

Form 1099-NEC is used to report nonemployee compensation paid to independent contractors. If you pay a U.S.-based contractor $600 or more during the tax year, you’re generally required to file this form with the IRS and send a copy to the contractor.

The key phrase here is “U.S.-based.” This form exists within the framework of U.S. tax information reporting — which means residency and location matter when determining whether it applies.

Do You Issue a 1099 to a Foreign Contractor?

Generally, no.

If a contractor is a non-U.S. person and the services are performed outside the United States, U.S. information reporting requirements — including Form 1099-NEC — typically do not apply.

IRS rules are based on two key factors:

- Tax residency: Is the contractor a U.S. person (citizen, resident alien, or U.S.-based entity)?

- Where services are performed: Were the services carried out inside or outside the United States?

When both answers point to “foreign,” no 1099 is required. That said, you’re not off the hook for documentation entirely.

What Documentation Do You Need Instead?

Skipping the 1099 doesn’t mean skipping paperwork. Proper documentation protects your business and demonstrates compliance if questions ever arise.

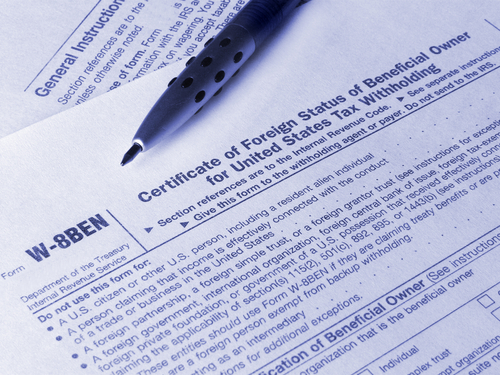

Form W-8BEN or W-8BEN-E

This is the most important document to collect from foreign contractors. Form W-8BEN (for individuals) or W-8BEN-E (for foreign entities) certifies that the contractor is not a U.S. person and is not subject to U.S. tax withholding.

Collect this form before making your first payment and keep it on file. It’s your primary evidence that the contractor falls outside U.S. reporting requirements.

Contractor Agreement

A written agreement defining the scope of work, payment terms, and the independent contractor relationship is good practice for any engagement — domestic or international. It also helps clarify that the work is being performed outside the United States.

Payment Records and Invoices

Keep organized records of all payments made, including invoices, receipts, and transaction confirmations. These support your accounting, help at tax time, and provide documentation if you’re ever audited.

When Might You Need to Issue a 1099?

There are situations where a 1099 may still be required, even for contractors based outside the U.S.

If the Contractor Is a U.S. Citizen or Resident Living Abroad

U.S. citizens and resident aliens are subject to U.S. tax obligations regardless of where they live. If your foreign-based contractor holds U.S. citizenship or a Green Card, you may still need to issue Form 1099-NEC.

If Services Are Performed Inside the United States

If the contractor travels to the U.S. to perform work — or delivers services considered to be “sourced” within the U.S. — reporting requirements may apply.

If Tax Residency Status Is Misclassified

Assuming someone is a foreign contractor without verifying their status is a risk. Always collect the appropriate W-8 form to confirm their status before making payments.

When the situation isn’t clear-cut, consulting a tax professional is the right move.

What About Withholding Taxes?

For payments to foreign contractors for services performed entirely outside the United States, U.S. withholding taxes generally do not apply. That’s the straightforward case.

However, exceptions exist — particularly when services are considered U.S.-sourced or when the contractor has U.S. ties. Form W-8 helps establish the contractor’s status and determines whether withholding is required.

Avoid making assumptions. Collect the W-8 form upfront, and if your situation involves any complexity, a tax advisor can help you verify the right approach.

Common Mistakes to Avoid

Even with a simple process, a few errors come up regularly.

Failing to Collect a W-8 Form

This is the most common oversight. Without it, you lack documentation to support your decision not to withhold or report. Make it part of your contractor onboarding process.

Assuming Location Equals Tax Status

Where someone lives and their tax residency are not always the same thing. A contractor based in Germany could still be a U.S. citizen — and subject to U.S. tax rules. Always verify.

Issuing a 1099 Incorrectly

Issuing a 1099 to a foreign contractor who doesn’t require one can create confusion for both parties and complicate their own tax filings. Get the documentation right first.

Not Keeping Proper Documentation

Even when no 1099 is required, documentation matters. Payment records, invoices, contracts, and W-8 forms should all be kept and organized.

Simple Checklist for Paying Foreign Contractors

Before processing a payment to an international contractor, run through these steps:

- Confirm the contractor is not a U.S. person (citizen, resident, or U.S.-based entity)

- Collect Form W-8BEN (for individuals) or W-8BEN-E (for foreign entities)

- Have a written contract or agreement in place

- Maintain invoices and payment records for your accounting files

- Consult a tax professional if the contractor’s status is unclear

This article is for informational purposes only and does not constitute tax or legal advice. Please consult a qualified tax professional for guidance specific to your situation.

Frequently Asked Questions (FAQs)

Do I issue a 1099 to a contractor who lives outside the U.S.?

Generally, no. If the contractor is a non-U.S. person and the services are performed outside the United States, Form 1099-NEC is typically not required.

What form should I collect from a foreign contractor?

Collect Form W-8BEN for individual contractors, or Form W-8BEN-E for foreign business entities. These certify their foreign status and support your decision not to withhold U.S. taxes.

What if the contractor is a U.S. citizen living abroad?

U.S. citizens remain subject to U.S. tax obligations regardless of where they live. In this case, you may still need to issue Form 1099-NEC. Verify the contractor’s status before assuming otherwise.

Do I need to withhold taxes when paying foreign contractors?

In many cases, no — if the services are performed entirely outside the U.S. and the contractor is a non-U.S. person. However, exceptions apply, and collecting a W-8 form helps confirm the correct treatment.

Should I consult a tax professional?

Yes. Tax rules vary based on individual circumstances, and the stakes are higher when international payments are involved. A qualified tax professional can help you apply the rules correctly.